TechBio at a Crossroads: Will It Learn from Digital Health’s Mistakes?

Software is not eating the life sciences and healthcare worlds…yet

I’ve spent the last 12+ months observing the TechBio industry and believe most industry participants are not learning the lessons of the Digital Health market’s failures to navigate the idea maze and follow the money. Let’s just say I have some hot takes after spending the last 3 years outside of the industry in consumer tech (YouTube/Google), and the 7 years prior to that in digital health (Verily / Google X Life Sciences, founded 2 digital health + AI startups).

Definitions, industry origins, and challenges

First some definitions:

TechBio: Software and computationally driven companies in the life sciences & biotechnology sector.

Digital Health: Software and computationally driven companies in the healthcare sector.

Both TechBio and Digital Health have:

entered the public consciousness in the early 2010’s (thanks to Benchling, Rock Health, a16z bio)

enthusiastic builder communities (Bits in Bio, Health 2.0)

taken advantage of digitization trends, both overall (shift to SaaS / mobile) and specific (HITECH act incentivizing adoption of EHRs in 2009 for digital health), though still have a long way to go

chronic challenges in monetization and value creation (biotech, healthcare providers and insurance still have minuscule IT spending)

Challenges in value creation

The problem is that software providers in biotech and healthcare don’t have a clear path to fast-growing (at least the hyper growth expected by VCs), sustainable and defensible monetization due to a variety of problems:

The purchasers of software often don’t have large purse strings to spend on IT, be it hospital systems or biotech, running at either razor thin (2% hospital operating margins) or negative operating margins (R&D organizations don’t spend much on data infra solutions when they need to generate data)

The decision makers (executives), influencers (doctors, scientists) and blockers (IT managers / sysadmins) are generally not very tech savvy

Sales cycles can drag for 12-24 months and revenue per seat may not justify these long lag times.

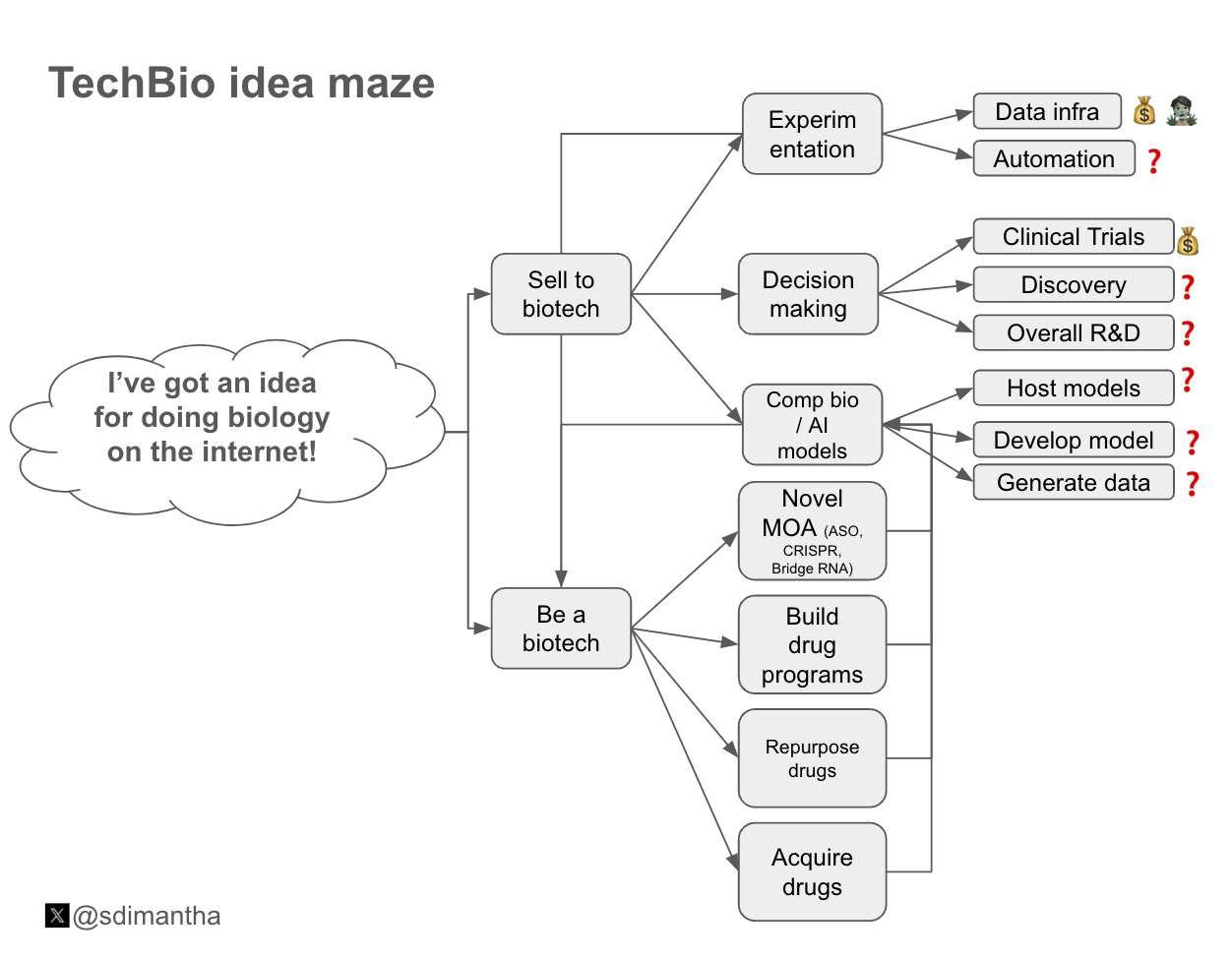

Mistakes navigating the idea maze

a16z partners Chris Dixon and Balaji Srinivasan popularized the “idea maze” concept, for example an idea maze on doing music / movies on the internet can be seen below:

From Startup Engineering, Balaji Srinivasan, Stanford University (2013)

Digital health companies and their operators and investors have made a handful of mistaken assumptions navigating the digital health idea maze that have led to the aforementioned challenges in value creation.

One mistaken assumption digital health companies made was apps + services can capture as much value as prescription drugs, at a fraction of the R&D risk and cost. This falls into two categories of companies, digital therapeutics and disease management programs.

Digital therapeutics: Omada Health was the most notable progenitor of the digital therapeutics trend with its hallmark digital diabetes prevention program for individuals with prediabetes to lose weight and drop their HbA1c (on order of ~$X00M in low margin revenue), however it pales by an order of magnitude compared to the value captured by Novo Nordisk’s GLP-1 portfolio ($15B in high margin 2023 sales from Ozempic, Wegovy). Outside of diabetes there have been some slightly less successful digital therapeutics in cardiovascular disease treatment; I pivoted my first startup into this category with a focus on high blood pressure treatment and high risk cardiovascular disease prevention. Some digital therapeutics apps have received FDA approval like Pear’s reSET for individuals with substance use disorders, but that did not save Pear from a bankruptcy sale for pennies on its previous valuation as uptake has been limited.

Digital disease management programs: Livongo was seen as the poster child of disease management programs with its landmark $18B merger with Teladoc in 2021, only to be almost completely written off as a $13.7B loss a year later with Teladoc valued at a mere <10% of its ZIRP era high. Some signs of hope can be seen in musculoskeletal per rabid investor appetite for Sword Health’s MSK at-home / remotely coached PT program, and mental health via Headway and Spring Health’s ability to make inroads with employers as employee engagement and cost saving solutions.

I see TechBio startups making similar and new mistakes, for example:

IT spending in discovery stage biotech is a low expense with limited growth at this time. Big pharma has larger budgets to spend on IT, but selling into big pharma is a long sales cycle even with new-fangled AI/ML solutions.

VC-funded TechBio startups pivot from selling computational / data platforms to biotechs to becoming a mediocre drug development firm, as per above they realize that IT spending on SaaS in biotech does not generate venture-scale returns.

One solution: full-stack startups and AI-first biotechs?

One potential solution to these mistakes and challenges navigating the idea maze is to create full-stack digital health and (AI-first) biotech startups that act like industry incumbents, but incorporate software & computational methods into the core of their operations with tech-native executives running the show. Why worry about sales cycles, budgets and buyers when you can become your own buyer? You can see this solution in action in insurance (Oscar Health, Clover Health, etc.), providers (One Medical, Forward Health), biotech (AI-first biotechs like Recursion, Exscientia, and others outlined in this 2023 AI Biotech report). However, full-stack company creation is a very capital intensive solution to drive value creation, as it requires much larger upfront CapEx and ongoing OpEx investments to stand up. While both digital health and biotech have examples of these full-stack companies, in today’s high interest rate world it may be hard to justify this type of investment.

Public market investors tend to agree by not placing a premium on these digital native versions of industry participants, for example full-stack insurance startup Oscar Health trades at a ~0.6x TTM revenue multiple (market cap $3.7B, TTM $6.5B) compared to UnitedHealth’s ~1.4x TTM revenue multiple (market cap of $524B, TTM $385B). However, full-stack companies can drive value in strategic acquisitions as can be seen by One Medical “trading” at a ~4x TTM revenue multiple (acquired for $3.9B by Amazon in 2023 on ~$1B in TTM) compared to Tenet Health at a 0.7x TTM revenue multiple ($14.8B market cap, with $21B in TTM revenue).

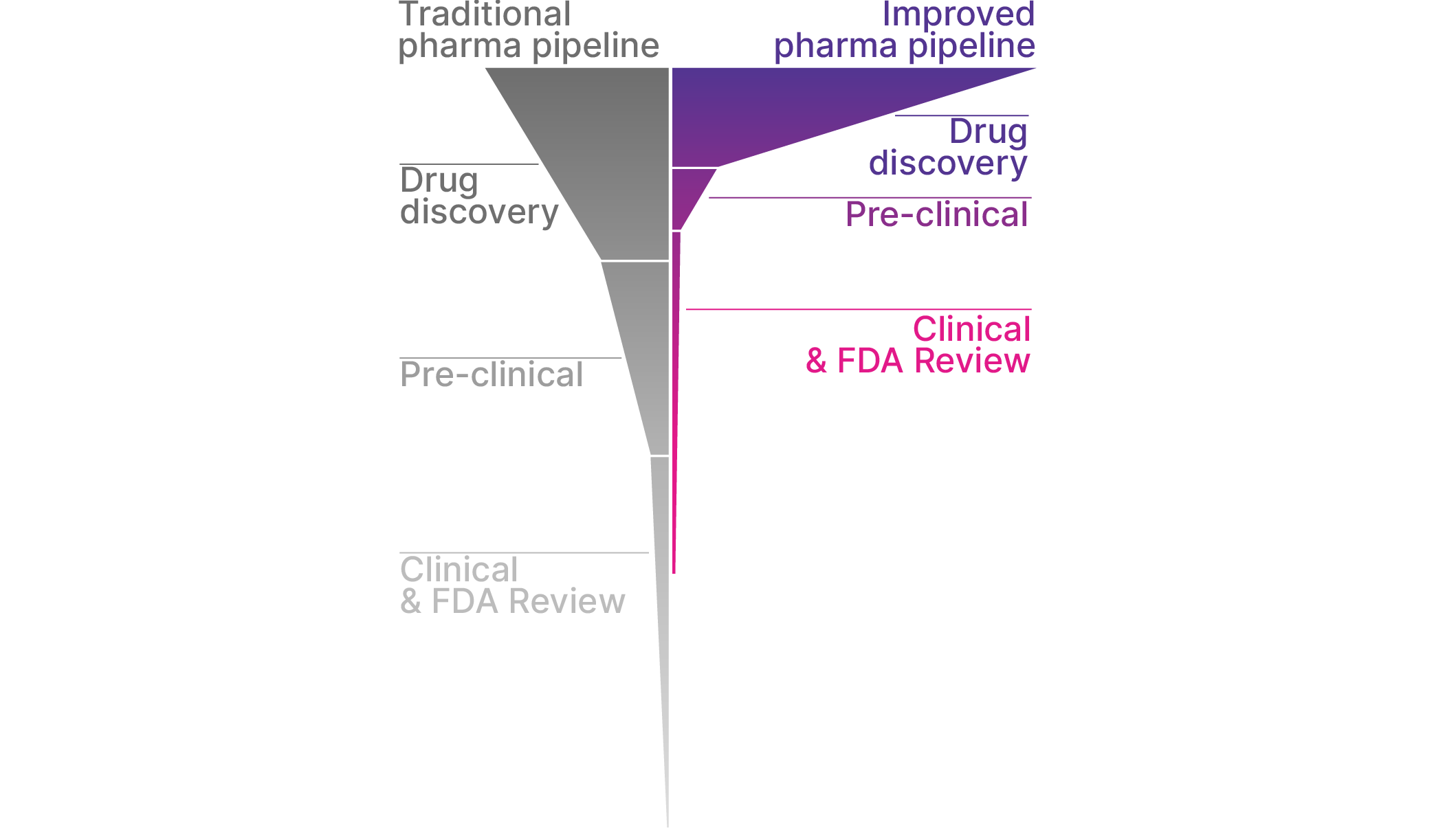

The market does not yet have any data points for approved drugs developed by AI-first biotechs to be able to place any sort of reasonable valuation/revenue multiple comparison, though Nimbus has been able to successfully sell two computationally designed clinical stage drug assets/platforms for ~$5B in cash, and it is worth keeping an eye on AI native biotechs with phase 2/3 assets like Recursion to see if an approved drug can emerge from Recursion’s re-shaped discovery funnel model.

Recursion re-shaping of the discovery & development funnel, though so far nothing has made it out the end yet

Other AI-native biotechs like Absci are trying to ride the GenAI/LLM narrative, with services like zero-shot antibody/protein design, however their TTM revenue $5.4M shows minimal uptake of this value proposition narrative so far. Generate Biomedicines CEO Mike Nally claims that generative design of proteins fundamentally changes the economics of drug development and other industry applications of proteins outside of life sciences.

Next time, the TechBio idea maze

The story of TechBio continues to be written, and I will share my thoughts on how companies can more successfully navigate the idea maze when the path forward is still foggy in my next post.