Venture Studio Models, continued: the history and formula for repeatable value creation

Can anyone recreate the productivity of Bell Labs, much less in healthcare?

I can’t stop thinking about venture studio models. Venture studios are basically companies that create companies, investing significant time capital in each venture in addition to a modest amount of financial capital, as opposed to venture capital firms that invest significant financial capital relative to time capital in each invested portfolio company. There is something seductive about the idea of creating a portfolio of companies/experiments that can systematize value creation and reduce risk in parallel over a shorter period of time than creating companies in serial like a solo entrepreneur/operator might attempt to do. Venture studios also embody the concept of ergodicity, which is another concept I find useful in many contexts. For more on the concept of ergodicity, and if you are a fan of Nassim Taleb’s antifragility, check out this post that also discusses portfolio theory and the Kelly criterion. Oh yes, I will be writing about complex systems in future posts.

In my last post I talked about the basic formula that consumer startup venture studio models employ, like Redesign Health does in healthcare. In this post I explore the history of venture studios more broadly, what has and has not worked in the quest to create value (specifically unicorn ($1B+ valued) companies), and what has been tried in healthcare (skip down / CTRL+F to the section labeled “Healthcare venture studios” if this is all you want to read). Unicorn companies are a bit of an arbitrary milestone compared to an exit (M&A, IPO, SPAC merger), but I’m using it for the sake of simplicity since it has entered the mainstream consciousness as a medium-term marker of success for startups.

The OG venture studios: Edison and Bell Labs

Venture studios are a new term for an old concept that started with Thomas Edison’s labs and perhaps has been in entrepreneurs’ minds since the invention of the corporation. Edison set up a laboratory in the late 1880’s to help invent and commercialize many ideas in parallel with commercializing the invention he is known for, incandescent lighting and DC electrification (with fierce competition from Tesla and Westinghouse). These ideas were often ahead of their time and included alkaline batteries, the phonograph, and the motion picture industry. Many of these ventures failed, but the main takeaway is that one successful value-creating invention (DC electrification / lighting) funds the rest of the venture exploration activities.

Bell Labs, founded by Alexander Graham Bell and formalized later in 1925, was a quick successor to Edison’s labs and employed some of the most brilliant people in the telecom/technology industry for decades including Claude Shannon, the father of modern information theory. Key outputs from Bell Labs include the transistor, laser, photovoltaic cell, Unix, C++, among many other technological advances and Nobel prize winners over the course of the 1920s to 1970s.

The formula here for both Edison and Bell Labs is to attract brilliant innovative people to work on hard science and technology problems that have industry transforming consequences.

Value creation =

(brilliant innovators)*(hard problems ∩ industry transforming potential)Corporate venture studios and ‘moonshot’ factories

Xerox PARC, founded in 1970, was the first successful attempt by Silicon Valley to recapture the spirit of Bell Labs, and created some of the modern value-creating innovations that have made computing accessible to the masses like the graphical user interface and mouse.

In the last 15 years, Google, Y Combinator, and others have tried to recreate this venture studio magic and for the most part have been funded by early successes (Google Search / Ads, YC’s early bet payoffs in Airbnb/Stripe/DoorDash/Coinbase/etc.) like has been the case for Edison and Bell Labs. Many corporations have tried over the years to recreate the magic of Bell Labs with little success, in part due to the Innovator’s Dilemma as articulated by the late Harvard Business School professor Clay Christensen. It is hard to disrupt your core business to focus on a relatively tiny problem, and that is why startups have time and again succeeded at fostering value creation where large companies have failed. Amazon is probably the closest any big tech company has come to fostering multiple value-creating innovations, but their last major hit AWS was founded 15 years ago.

The formula here is largely the same as Edison and Bell Labs for Xerox PARC, however for large companies the focus is on financial value creation for shareholders as opposed to industry transformation.

Value creation =

(brilliant innovators)*(hard problems ∩ company value transforming potential)Venture studios in the internet era

Bill Gross (not the PIMCO founder Bill Gross) attempted to bring back the spirit of Edison Labs with Idealab in 1996, which claims to be the “longest running technology incubator”. Apparently Coinbase is one of their companies, which would qualify as their largest value-creating company by many orders of magnitude (currently at a ~$60B enterprise value), but I do not know at what stage Idealab got involved. Bill recently went on a PR push celebrating 25 years of Idealab’s existence with 25 lessons, and these lessons are worth a quick perusal even though there is a lot of overlap with the Lean Startup thinking that Eric Ries and Steve Blank have promoted over the last decade or so (“iterate like crazy”, “be lean”, “find product-market fit”, etc.).

More modern takes on the venture studio concept include:

Atomic (SF), founded in 2012 and run by close Peter Thiel affiliate Jack Abraham and with a company that has a qualifying and largest value-creating event in Hims & Hers that recently SPAC-IPO’d to the tune of a market cap of ~$1.9B in just over 3 years (and who can forget those NYC subway station / car ads).

Prehype (NYC), founded in 2011 and whose largest value-creating company is Hims & Hers competitor Ro (currently valued at $5B)

Betaworks (NYC), founded in 2007 and whose largest value-creating company is probably Giphy (acquired by Facebook for a reported $400M)

Expa (NYC/SF), founded in 2013 by Uber co-founder Garrett Camp and whose largest value-creating company is Forward (valued at $1B after most recent fundraising).

Axiom Zen (Vancouver), founded in 2012 and whose largest value-creating company is Dapper Labs (the creators of NFT-based games Crypto Kitties and NBA Top Shot and currently valued at $7.5B in recent fundraising talks). I am particularly fascinated by Dapper Labs, and will go into my thoughts on NFTs, Ethereum, and the long tail of crypto value creation in a future post.

Other venture studios, which I won’t go into, but luckily someone else has in the linked article

I would argue that modern venture studios are creating large amounts of financial value (similar to large company formula for value creation), but with a focus on attracting top operators, focusing on medium difficulty problems and generating value for LPs. These venture studios also do not produce anywhere near the same level of societal/industry transformation value that their predecessors (Edison, Bell, Xerox, etc.) have done in the past.

Value creation =

(highly skilled operators)*(medium difficulty problems ∩ LP value transforming potential)Healthcare venture studios

If you made it this far, thank you, and this is where I finally talk about venture studios in healthcare. Do you notice a trend in recent venture studios that I listed in the previous section? Yes, the largest value-creating companies for 3 of the 5 modern venture studios I listed are healthcare/healthcare-adjacent.

The main value of venture studios in healthcare is to mitigate risk, specifically two types of risk: market/commercial risk and technology risk. The former is more important to areas like digital health / health IT and healthcare services (technology is easy to implement, however reimbursement/commercial path is not well established), and the latter is more important to biopharmaceuticals and medical devices (market need is clear, however technology has not been developed).

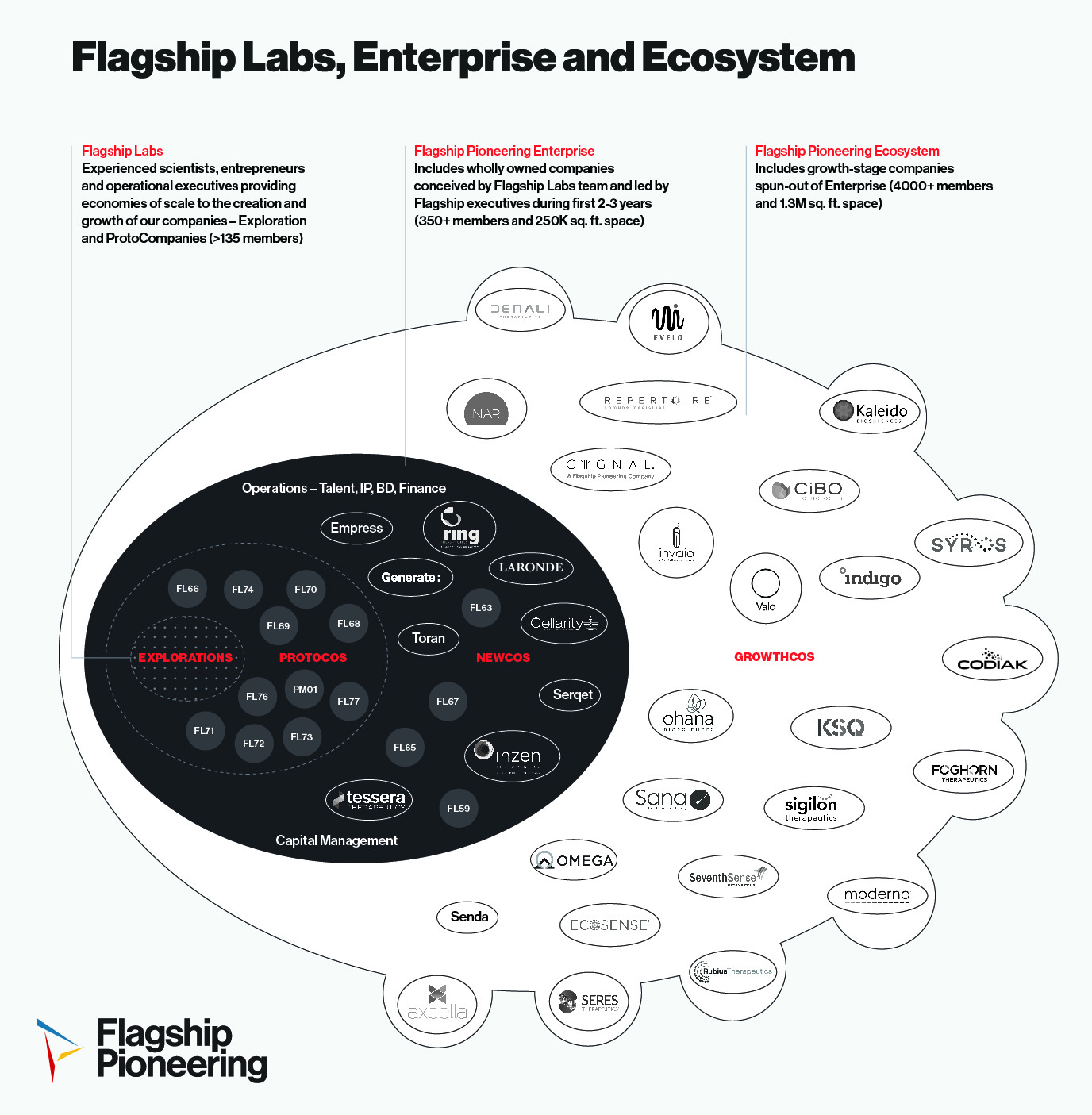

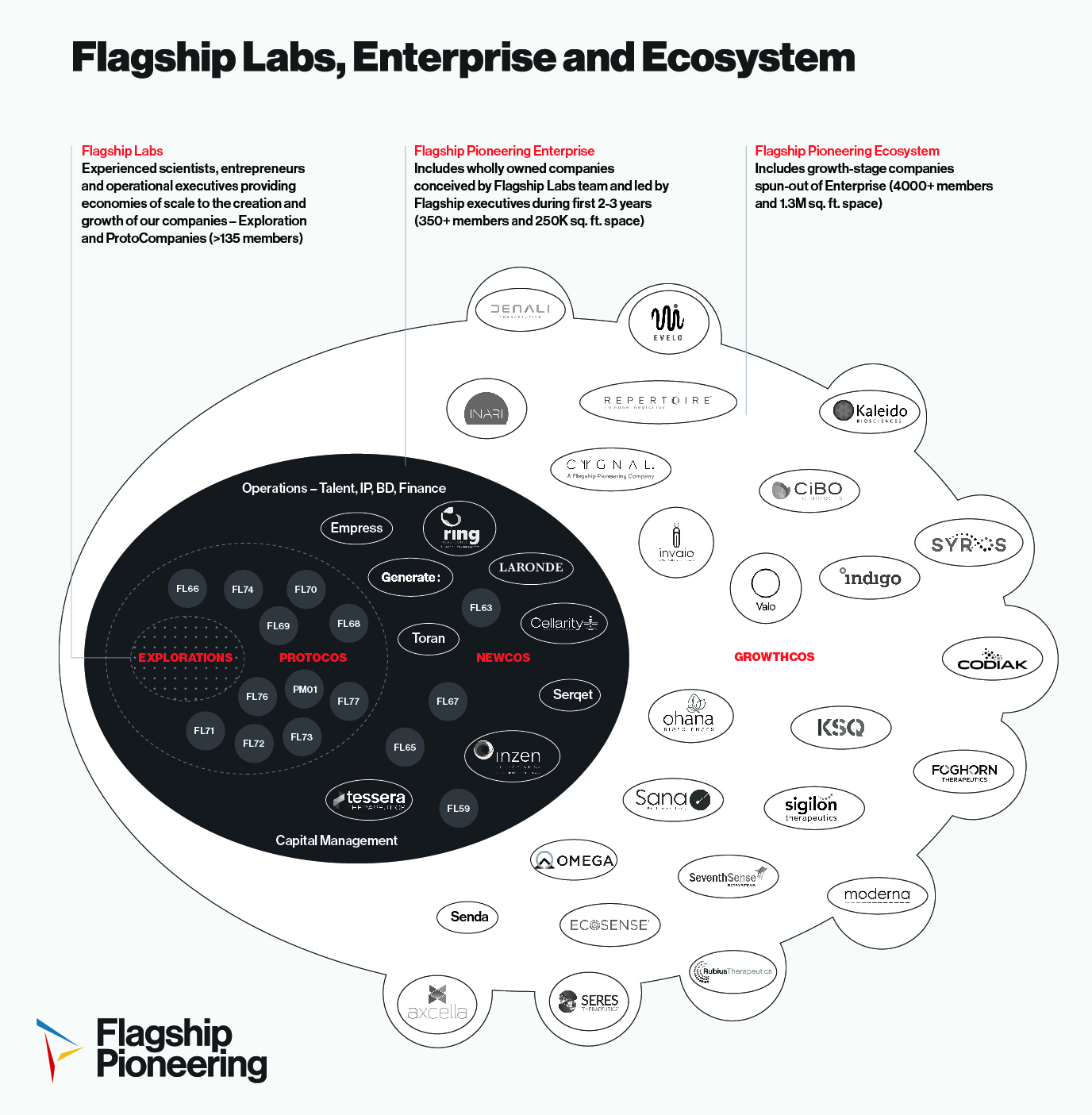

Flagship Pioneering was one of the first venture studios in healthcare focused on biotech innovation, and reducing the first type of technology risk via a venture studio model. Flagship’s model is to vet multiple ideas per year internally (Explorations), seed some of the best ideas with $1M over 1 year (ProtoCos), commit capital and shared services to those seeded ideas that are the most promising candidates (NewCos), and raise external funding for the most promising of those promising candidates (GrowthCos). Their biggest outcome to date is the mRNA platform company Moderna, which has a total enterprise value of ~$58B and was one of the winners of the pandemic’s vaccine response, and has returned at least $4-5B and 30-40x to Flagship on their original investment per their reported holdings as of the end of 2020. Moderna was both a financial coup for Flagship and a huge net positive contribution to society to help us escape the COVID-19 pandemic. My bet is that Flagship’s next big outcomes in its ecosystem will also be in platform companies like AI-powered biopharma company Valo and biotech manufacturing company Resilience (not a portco, but the CEO was briefly a Flagship operating partner). I plan to dig into how AI is improving pharma R&D success rates within their own portfolios in a future post dissecting Recursion Pharmaceuticals’ recent S-1 and IPO and competitors following close behind like Valo.

I sure hope those extracellular vesicles housing those GrowthCos are all as value accretive as Moderna has been. Source: Flagship Pioneering ecosystem diagram

{kind=link}

Value creation =

(reduce technology risk)*(subject matter experts)*(highly skilled operators)*(unmet identified patient needs ∩ LP value transforming potential)On the second market uptake risk side, private equity has been heavily involved. Accretive is a New York-based general venture studio, whose biggest value-creating outcome to date seems to be R1 RCM (f/k/a Accretive Health), a revenue cycle management company that once got into a tiff with Al Franken over debt collection practices and recorded $1.3B in 2020 revenues with an enterprise value of ~$7B. Accretive preaches its tenet of creating a “value edge”, which seems a bit obvious, but better than a tenet of creating “value destruction”. Aside from having some partners with interesting histories (including Edgar Bronfman, Jr., who inherited a multibillion dollar company in Seagram, was convicted for insider trading, and was a Broadway/film producer / songwriter among other quirky characteristics). If Accretive feels like a private equity firm, you are not mistaken, because it is effectively a private equity firm disguised as a venture studio. One of Accretive’s most successful alums is Adam Boehler, who in turn has founded a in-home medical provider with a reported $3.5B exit to UnitedHealth and has created his own venture studio called Rubicon Founders (Nashville-based), presumably with PE backers again with a reported focus on everything from senior living to genomics to the formation of payviders.

Accretive’s definition of value edge. I would hope value is not doing nothing, but maybe we are all creating a value edge then? (Source: Accretive’s website)

Finally, we get back to Redesign Health. Redesign seems to have been formed after seeing success in silently funding/incubating Candid, a slightly more expensive Smile Direct Club competitor that has taken advantage of performance marketing as Ampush founder and Redesign advisor Jesse Pujji describes in his recent podcast interview on Invest Like the Best (at ~the 1:05/-0:29 mark). Redesign has raised about $250M, plans to create 50+ healthcare startups, and employs about 56 people. Clearly, they have a different management fee structure than your typical venture fund in order to support this level of headcount.

To recap from my last post, my take on the Redesign Health formula is the same as the formula I believe modern venture studios focused on creation of consumer startups use to primarily reduce the commercial/market uptake risk:

Develop investment theses in un/under-addressed areas in healthcare ideally with a consumer focus and potential for recurring subscription revenue streams

Raise money from LPs

Invest in branding and experience design (maybe this step happens before by using a landing site to develop conviction in a given thesis with FB ad spend)

Incorporate startup(s)

Recruit experienced (sometimes overqualified) operators who want to be CEO of a startup with equity upside

Acquire customers using Facebook/Google ad spending

Raise money from outside investors based on LTV proof

Rinse and repeat

Gain efficiencies across companies from studio model (??)

Create celebrity-backed SPACs to acquire the companies and take them public - like Atomic did with hims&hers

I’m long on the venture studio concept in healthcare and firmly believe there is more opportunity to iterate on the above value creation formulas to create significant additional value and mitigate risk of the probability of this value creation, specifically in consumer digital health / telehealth, value-based care, and biotech + biotech-affiliated areas among other areas.

What an insightful post!

This is incredibly insightful!